Optical equipment sales in tough times

Carriers are spending money, but newer suppliers face sales hurdles.

By KATHLEEN RICHARDS

The communications revolution ran into a "bit" wall in 2000. Investors pulled back, capital dried up, and revenues from data services didn't sustain the networking systems required to support them. With capital harder to come by in 2001, many service providers have modified their business plans to increase profitability, conserve resources, and use current systems more efficiently.

Equipment sales in this environment are challenging. Traditional systems vendors such as Nortel Networks, Lucent Technologies, and Cisco Systems-the bellwether companies for fiber-optic networking and, in the case of Cisco, the technology sector-are reporting record losses. Many didn't see the slowdown coming and most are cautious about the timing of a recovery. Cisco expects some stability in the first quarter of 2002.

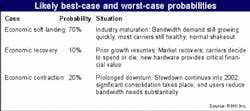

For newer companies, especially startups, the landscape is even bleaker. "The target market that was hopping on new technologies from startup companies has diminished greatly," states an August 2000 report by Grier Hansen, analyst of optical infrastructure and carrier infrastructure at Current Analysis (Sterling, VA).

But carriers are spending money. Competitive local-exchange carrier (CLEC) XO Communications Inc. (Reston, VA) is making some modifications to its equipment purchase and network expansion plans this year after investing heavily in its infrastructure for two-and-a-half years. The CLEC, which has undergone a lot of changes over the last four years, today operates metro fiber-optic loops and offers voice and data services across 62 U.S. cities.

In 1997, XO merged with Concentric, adding an OC-3 backbone, shared Web hosting environment, and some DSL customers to its local-exchange services. Around the same time, XO bought into the long-haul intercity market through an agreement with Level 3 Communications and added wireless licenses. During these last two-and-a-half years, XO has introduced multiple new technologies into its networks. The carrier plans to converge voice and data onto a common transmission platform and upgrade the voice-switching system to soft switch technology. DWDM, Gigabit Ether net, and wireless systems have been added to the metro markets. Networks once populated primarily by Nortel's optical transmission and switching equipment now feature routers and switches from Cisco and ONI Systems and softswitching technology from Sonus Networks.

"All of that is still cranking along as we set out in our strategic technology plan in 1998," says Doug Carter, chief technology officer at XO Communications. "The intercity system is being hooked up; we've got a bunch of softswitches installed and we're starting to transfer traffic to them. We've expanded the IP backbone from OC-3 to OC-12 and we'll be upgrading it to OC-192 in the last quarter of this year. The only significant change we've made was not in the design but in the way that we've implemented the intercity wavelength structure."

In the process of connecting its intercity loops in early 2001, XO Communications decided to adopt a wavelength leasing strategy rather than light fiber to conserve capital. The carrier also put its plans to expand into European metro markets on hold.

"We have ownership through an IRU [indefeasible right of use] of intercity fibers through Level 3 and a spare conduit," says Carter. "We had planned on and actually had started to light those intercity fibers with a Ciena Corestream DWDM 10-Gbit/sec wavelength system earlier in the year when Wall Street did its little flutter and pullback. We decided not to light the intercity system this year, but rather lease wavelengths, basically share the intercity wavelength system with Level 3 until next year or the year after.

"Most of our capital [today] is in what we call 'success-based capital'-that is, extensions to the metro fiber on a per-customer basis as we add more customers and that continues unabated."

XO also opted to defer the purchase of an OC-192 laser system, about a $125-million component, until sometime after this fiscal year. And while the carrier is leasing wavelengths for its intercity network, it is still purchasing all of the service generating and multiplexing equipment required to turn up that network.

Most carriers have development groups staffed with engineers that focus on next-generation technologies. In XO's case, that means voice transport, voice switching, and data services and voice services.

"We've got a steady stream of existing suppliers, large-scale system integrators like Cisco and Nortel and Lucent and so forth that talk to us about changes in their product line," says Carter. "We also have smaller companies that are trying to break into various spaces that come in and talk to us. There is little likelihood that we are going to select a significant number of vendors over the next year because we have made an awful lot of big selections in the last 18 months."

The focus at XO right now is on getting its current network properly implemented. Next year, the carrier's capital spending, like this year, will be allocated to "success-based capital" because so much of the infrastructure is already built.

At this point in the carrier's maturity, XO cannot afford to take a chance on complete greenfield startups for substantial critical functions of the network, asserts Carter. "If a company comes in and they've got a very neat idea about something, we tell them, 'We think this is very cool, you probably ought to go talk to one of the big system integrators about maybe being an OEM and taking responsibility for all those things that a startup has a hard time doing while supporting the national deployment and maintenance of their products. We do entertain that.

"Three years from now, I would expect that we'd be singing a slightly different tune. We'll have the basic foundation of the network well enough established and built that we'll be a little more cavalier about experimenting with new companies with new technologies on the fringe, but it is not timely for us. Now, it probably is for other companies that are older," says Carter.

Many manufacturers have focused their sales efforts on the established incumbent carriers, partly because the financial future of many CLECs and other emerging carriers is unclear. A conservative bunch at best, incumbent carriers tend to stick with the larger system vendors with proven technology and a solid financial history, especially in an uncertain climate. But as networks continue to evolve, the convergence of voice and data services onto a protocol-independent infrastructure and the promise of all-optical networking are opening the door to newer vendors with emerging technologies.

Verizon Communications (New York City), which formed in June 2000 when GTE and Bell Atlantic merged, will invest $12.5 billion in its wireline infrastructure this year and $5 billion on wireless-in all, $1 billion less than what the company spent in 2000. Domestically, the communications giant offers local-exchange, long-distance, Internet access, and data-networking services in 31 states, the District of Columbia, and Puerto Rico. According to company spokes person Ells Edwards, Verizon is investing about half of its designated $12.5 billion for wireline in legacy equipment and the remainder in newer technologies. "The majority of it is being spent on metro," he says.

Verizon is headed toward a field trial of an all-optical core in the middle of next year. Engineers at the carriers' optical-networking lab are currently in the process of doing tests of this technology. The team is responsible for architecting, designing, and field-trailing the optical-networking technologies. Many suppliers in the core optical-network space are startups getting their first-generation products out the door, notes Dean Casey, director of next-generation network backbone for Verizon Labs (Waltham, MA).

Today, Verizon Labs personnel evaluate many technologies at an earlier stage of their development. "We would like to know if we can buy best-of-breed, for example, in products that have to interwork, so we are very interested in testing best-of-breed switches, grooming equipment, DWDM, a whole range of products to see if these products will in fact interwork," says Casey. "We are putting various services over these [individual elements and systems] to see how they work. We're doing cost analysis on alternative approaches such as ring or mesh configurations of the network. We're looking at the reliability and stability of these products, in particular where we are looking at younger, less mature vendors."

The reliability of the new technology is critical from a quality-of-service standpoint. Telcordia OSMINE certification is required to ensure that any equipment put into the network is compatible with the operations support systems. Equipment must also be NEBS Level 3-compliant.

In the optical-networking space, the Waltham lab is evaluating technologies that may be two or three years away but less intensively than the more mature technologies such as photonic switches based on micro-electromechanical systems (MEMS). "We're doing experiments now in the laboratory using late beta-phase equipment that we expect to become generally available in the first or second quarter of next year, which we will then roll out into field trials in midyear," says Casey. "Following that, there might be first office applications depending on how the field trial goes. The process moves from the laboratory to field trials to first office applications. I think for Verizon, you will see a lot more of that."

Interoperability, reliability, on-time delivery, and pricing are all key considerations in the procurement process. A large number of vendors make direct contact with incumbent carriers such as Verizon.

"What we find is that there is a lot of difference between what is said on the marketing side and what we actually receive from vendors," says Casey. "When push comes to shove, you do have to get the equipment in and kick it around to see if it really works. Often, you find a product that is marketed very actively is not really available. When you finally do get it into the laboratory, it's usually in an earlier state of development than the manufacturer represents, especially for the younger companies.

So it's very important to get a look at a product in an early stage. What's happening is it's pushing developers to accelerate their development cycle and it is pushing us to accelerate our deployment cycle, and we have to find efficient ways of doing that," says Casey.

Even though many vendors are targeting the incumbents, these companies should also focus on the smaller carriers and, if in the position to do so, international markets, advises Current Analysis analyst Hansen.

Riverstone Networks Inc. (Santa Clara, CA), a supplier of routers and switches for MANs, has its technology deployed in about 40 countries, through channel partners and its own international sales team. The vendor uses basically a three-pronged strategy when it enters new markets.

First, Riverstone hires local salespeople who understand the customer base. A speaker of the native language is not sufficient. The local sales team should already have contacts within the local telephone companies.

"You can't run an international business from your cube," says Stephen Garrison, director of corporate marketing at Riverstone Networks. "Relationship selling is far more important overseas than in the states where you can get a lot of business based on the technology." Websites in the native language also can help. Riverstone has native Websites in Japan, China, Korea, and parts of Europe.

It is also important to devise a worldwide branding scheme that the local market can understand. River stone touted "bandwidth with brains"-basically, equipment that helps create services from raw bandwidth. "Bandwidth with brains" worked in Europe but did not make sense to Asians. So Riverstone changed its tag line in Asia to "enabling service providers' infrastructure," a phrase that the local markets understood.

The third key element is understanding the timing of the market, which requires a lot of research up front. There are two phases to the metro. Phase 1 is creating duplicate content so the content is closer to the customer. Europe still has significant data-center business, as does Latin America, while in the United States, this market "is largely over," says Garrison.

As Current Analysis's Hansen states in his report, "Not all startups are going to make it through these rocky times-and some of the casualties will be companies with good product. The best bet for survival is to adapt to the changing economic climate and its effect on purchasing behavior, focusing on smaller customers and diverse markets for short-term revenues while continuing to pursue longer-term opportunities with ILECs [incumbent local-exchange carriers]."