Favorable climate for fiber-optic cable deployment worldwide

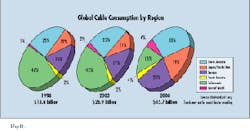

North America led cable consumption worldwide with a 25% share, or $3.4 billion, in 1998. Proliferation of the shorter cable links used in premises-data and local-loop networks will drive future growth in the North American cable market, which is expected to reach $11.9 billion by 2008. Europe ranked second in fiber-optic cable usage in 1998, with 15%, or $2.1 billion. European cable consumption is expected to reach nearly $9 billion in 2008.

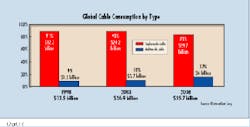

Singlemode-cable consumption, estimated at $12.3 billion in 1998, is forecast to reach $29.7 billion in 2008 (see Fig. 2). It dominates the global market, where its primary use is in telecommunications networks. During the 10-year period, however, its market share will drop from 91% in 1998 to 83% in 2008, as multimode cable gains market share.

Multimode-cable use, dominated by North America, will grow from $1.2 billion in 1998 to $6 billion in 2008. North America's market share is significantly higher than that of other world regions for the following reasons: earlier applications of fiber optics in local-area and wide-area networks, rapid expansion of premises interconnects, and the use of fiber optics within other equipment such as switches and automobiles. Parallel optical interconnect components-multifiber connectors, cable, and vertical-cavity surface-emitting lasers (VCSELs), which are being phased into production equipment-will drive the fast-growing market for short interconnect multimode fiber links.

Optical-fiber deployment remains the backbone of communication network capacity expansion, despite the current excitement about dense wavelength-division multiplexing (DWDM) and the push toward higher data rates in time-division multiplexing (TDM). In a new build, the cost of deploying a high-fiber-count cable is little more than the cost of deploying a low-fiber-count cable.

Moreover, the price of singlemode cable in North America dropped to 8 cents per cabled fiber meter in 1997 to 1998, from 10 cents in 1995 to 1996. This significant price drop is due in part to manufacturing expansion by major suppliers. Many telephone companies locked in multiyear cable contracts at these lower rates.

The economic advantages of DWDM apply when this technology is used in built-out networks that do not have many unused fibers or in networks where the cost of deploying new fiber cable is prohibitive-for very long spans or when there is a requirement to trench fiber into place.

These conditions exist in many long-distance interexchange carrier networks. Some carriers have "lit" almost all their fiber, exhausted leasing options, and moved to relatively high data rates. In these cases, DWDM is an obvious solution.

Many local-exchange carriers (LECs), on the other hand, deal with short fiber-cable spans of 5 to 50 km. These carriers now use OC-48 (2.5 Gbits/sec) or low-speed data transmitters as a viable option. Often, there is a need to deploy additional fiber in the local loop in Synchronous Optical Network/Synchronous Digital Hierarchy (SONET/ SDH) rings, mesh networks, or other configurations to increase overall network reliability. As a short-term solution, TDM, new fiber deployment, or a combination, often is a more economical choice for LECs than DWDM.

The principal difference among singlemode fibers is their dispersion characteristics. Fiber dispersion broadens the signal pulse as it travels along the fiber. The longer the transit, the more the pulse broadens. At higher data rates, pulses are closer together and can tolerate less broadening before one smears into the next. Therefore, fiber that has zero dispersion at the transmission wavelength is ideal.

Conventional singlemode fiber had been standardized with zero dispersion in approximately the middle of the 1310-nm band. Dispersion typically increases as the wavelength increases, so in the 1550-nm region, this conventional fiber has very high dispersion. This description fits most of the fiber deployed worldwide.

To correct the problem of high dispersion in the 1550-nm region, nonzero dispersion-shifted fiber (NZ-DSF) was introduced. NZ-DSF puts the dispersion zero in the middle of the 1550-nm band, which makes it ideal for high-speed data transmission using a single wavelength. Unfortunately, trying to operate a DWDM array across the entire 1550-nm band, with negative dispersion in half the band and positive dispersion in the other half, creates major problems in the system.

NZ-DSF, which places the dispersion zero at the edge of the 1550-nm band, makes DWDM deployment more feasible. However, NZ-DSF represents only a tiny percentage of deployed singlemode fiber worldwide.

The rapid expansion of telecommunications networks is creating export opportunities for fiber-optic cable suppliers from North America, Europe, and Japan/Asia-Pacific. Trends toward freer trade policies, reduced variance between worldwide interest rates, and the liberalization of telecommunications globally are fueling the rapid expansion of communications networks.

But to counter threats to their unregulated operations and compete through subsidiaries in the global marketplace, telecommunications pro viders have instituted dramatic reorganizations aimed at reducing operating costs. While this new emphasis on cost control has had little impact on installation and upgrading of long-distance and inter office trunks, it has significantly slowed the extension of fiber optics into the local-loop feeder and distribution networks.

Unlike telecommunications, data-communications fiber optics requires high-performance cable, but it can tolerate greater fiber loss and shorter device lifetimes. The emphasis in data-communications components-especially those operating below 155 Mbits/sec-is on high-volume production of standardized components at low cost (to compete with copper and wireless). Since fiber loss is not critical, short-wavelength gallium arsenide-based optoelectronics with multimode fiber can satisfy most requirements. In contrast, the optimal cable assembly for telecommunications uses indium phosphide-based long-wavelength optoelectronics and singlemode fiber. Thus, this market will favor suppliers with automated high-volume cost-controlled production facilities.

The marketing challenge for data communications is also different from that of telecommunications. With data communications, system integrators play a key role in designing and implementing the network; most customers do not have the necessary engineering and installation expertise within their own organizations.

Because hundreds of component types must be provided to tens of thousands of end users, distributors will become the dominant channel in the private-data-network components market, whereas direct sales is used in the telecommunications sector. Value-added resellers (VARs) or system integrators who assemble cable links and other elements into network packages will often also act as distributors. The more successful component suppliers, therefore, will be those adept at managing and supporting sales through distributors.

As optical-fiber use in premises networks grows globally, the number of cable-assembly operations will increase. These companies can quickly turn around cable assemblies. Although some distributors may play this role, increasingly they are relinquishing this capacity to cable-assembly shops.

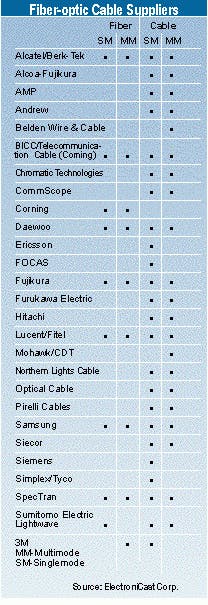

Some companies design, produce, and sell practically all that goes into the network: fiber, fiber cable, connectors, apparatus, optoelectronics, passive optics, and the equipment that incorporates these elements. This capability provides leverage in developing high-value, long-term supply packages within the strategic partnership framework. Major global cable competitors are listed in the Table.

Over the next decade, global fiber-cable consumption will continue to grow despite slowed momentum as the market reacts to a sharp decline in the suboceanic segment. Multimode-fiber cable will gain market share as fiber infiltrates the premises arena. While DWDM offers an economical solution in cases where providers have exhausted other fiber resources, most of the conventional singlemode fiber deployed worldwide has high dispersion in the 1550-nm region. NZ-DSF solves the problem, but to date, it represents only a small percentage of the fiber installed worldwide.

Global competition in the telecommunications and data-communications markets will continue to fuel fiber-cable sales, although the sales channels will differ for each market. To succeed, component suppliers need to support sales through distributors for the data-communications market. Finally, suppliers that offer complete cable-assembly solutions are well-positioned in the global market.

Stephen Montgomery is president and Saba Hailu is a senior analyst at ElectroniCast Corp., a market-research firm based in San Mateo, CA.