Have the stalwarts lost the ability to innovate?

Jeff Lipton, Chase H&Q

Last year was stellar for virtually any stock associated with optical communications. Almost without exception, every public name in this space has outperformed the broad technology indices, with stocks like SDL and JDS Uniphase appreciating an astounding 1,000% and 830%, respectively, during the year. Valuations have escalated as optical plays continue to beat Wall Street projections, reflecting the strong fundamentals of the industry. Meanwhile, the technology market at-large performed phenomenally well due to a variety of factors, providing a favorable environment.

It doesn't hurt either that most investors acknowledge that we're in the early stages of a huge optical-market opportunity and that the markets have become less sensitive to high valuations. Rather than waiting for the day when a company achieves its profit potential and bidding up the stock accordingly, investors are now willing to pay up-front as long as the vectors are pointing in the right direction. Sycamore Networks perhaps best illustrates an early-stage equipment play whose valuation reflects its potential rather than its current financial performance.

Armed with valuable currency, industry stalwarts such as Cisco Systems, Nortel Networks, and Lucent Technologies are on acquisition tears to fold in best-of-breed product lines from companies such as Cerent and Qtera, faster and arguably better than they could develop these solutions internally. Smaller system vendors such as Ciena and RedBack Networks are maximizing their high market caps as well, adding new capabilities and broadening their total addressable markets with acquisitions such as Lightera, Omnia, and Siara Systems.

For somewhat different reasons, component suppliers are scrambling to broaden their product offerings to become one-stop shops and move up the value chain, providing modules as well as components. Uniphase best exemplifies this trend, first merging with JDS Fitel and later swallowing Epitaxx, OCLI, Sifam, and Oprel-all in the span of a single year.

What's remarkable is not only the rate of these acquisitions but also the market's acceptance of jaw-dropping valuations. Uniphase paid only $45 million for IBM's Zurich 980-nm pump laser operation in 1997 and $180 million for Philips's optoelectronic business in 1998, two operations that would undoubtedly command much higher valuations today. Even earlier in 1999, the $550-million acquisition price for Lightera seemed remarkable but now pales in comparison to the $7 billion paid for Cerent and the $3.25 billion paid for Qtera.

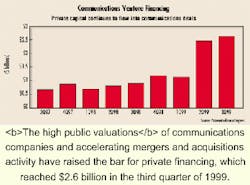

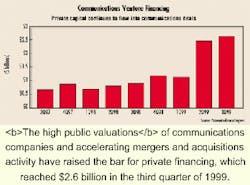

Escalating valuations and their causal factors haven't been confined to public plays, either. High public valuations and accelerating mergers-and-acquisitions (M&A) activity have raised the bar for private financing, as well (see Figure). The record is held by Corvis, a private company that recently closed a financing round with a post-money valuation in excess of $2 billion.

Not only are higher public valuations fueling this M&A frenzy, but changing investment behavior also is playing a role. The market is now emphasizing top-line growth and valuing most emerging communications plays on a revenue multiple basis. And most investors don't draw the distinction between organic and acquired revenue. The shortest route to new-product revenue, and consequently new growth, is to buy another company, rather than design the product internally.

Of course, profitability still matters, but the most relevant measure is now profit net of charges. Investors and analysts no longer adhere to generally accepted accounting principles (GAAP) as strictly as they once did. Many companies now report their earnings two ways-pro forma and GAAP-and the market pays attention to the pro-forma numbers. Even the long-expected disappearance of pooling-of-interests accounting, which will force acquirers to write off huge charges and widen paper losses, won't slow things down. So there's some truth to the theory that it makes economic sense to outsource research and development to the startups, while the large system vendors control the customers and manage the process. As a result, the use of M&A is now an accepted method of growing the top-line, thereby enhancing valuation, as long as it makes strategic sense and isn't too dilutive to pro-forma earnings.

Beyond the financial mechanics of funding new projects through acquisition, and aside from taking advantage of an extraordinary valuation environment to accelerate time-to-market or add a key product line or capability, mature players may be pursuing the M&A route partly because it is becoming harder for these companies to innovate. Anecdotally, it seems that a higher proportion of the groundbreaking new products come from startups. Take ultra-long-haul dense wavelength-division multiplexing systems, for example. If Nortel had quickly been able to translate its research on dispersion-managed solitons into a marketable product, it would not have paid the price for Qtera. Similarly, implicit in Corvis's high valuation is the assumption that the startup could potentially out-execute Ciena and Lucent when it comes to next-generation long-haul systems.

While a large proportion of the current innovation is attributable to the household names, the environment is changing rapidly, and these companies are finding it difficult to remain the leaders. A large part of the problem lies in human resources. It's becoming harder for established public companies to retain their most talented physicists and engineers.

As recently as a few years ago, start ups as a group were riskier than they are today. For one thing, working at a startup meant a lower salary but greater potential upside in the form of stock options. Startups were also less accepted as a stimulating engineering environment. People that favored state-of-the-art atmospheres gravitated toward places like Bell Laboratories.

But the amount of venture money flowing into startups and the trend toward M&A have changed this environment. The risk profile of startups, in general, is no longer what it was. Many private companies can now afford to pay top-talent competitive salaries in addition to stock options. Some startups can also afford to invest in cutting-edge facilities. As larger companies become more willing to use their market capitalizations to acquire and, conversely, as acquisition gains popularity as an exit strategy for startups, the risk of failure for new players is diminishing somewhat. As a result, the top tier of startups offers a great environment for innovation that can yield enormous financial upside with less risk than ever before. Consequently, it's becoming harder for established companies to compete for the top talent needed to innovate.

The implications of this new environment are hard to quantify. But as long as the market holds up and venture capitalists fund new companies at unprecedented levels, M&A activity will continue and more of the engineering workforce will migrate to early-stage suppliers. To remain competitive, more mature vendors will need to balance internal innovation with a well-executed acquisition strategy. M&A should be used selectively to gain new products and capabilities quickly; the current market environment rewards a sharp M&A strategy.

Acquisition clearly can't replace internal innovation entirely, however. Should large companies lose the ability to innovate, they will become nothing more than distributors. Furthermore, the cost of M&A is high, especially if we consider the proportion of acquisitions that will ultimately fail.

If we look at professional baseball for a parallel, can a team succeed for more than a season or two if it gains all of its talent through free agency, vying with all of the other teams to pay up for the Ken Griffeys of the league? Or is the team more likely to be a long-term winner, not to mention more cohesive, if it develops promising young players internally, such as a Derek Jeter or a Pudge Rodriguez, and brings in a few heavy-hitting free agents from time to time? I'd argue that there's something wrong if we have to buy all of our talent.

Jeff Lipton is an equity research analyst for Chase H&Q (San Francisco), covering photonics and broadband components. He can be reached at (415) 439-3280 or [email protected].