Promise of ATM-grade IP network convergence

The migration from legacy to IP/MPLS networks is causing the telecommunications industry to reach a major inflection point. Investments by service providers in ATM and Frame Relay (FR) networks, which still support profitable data services, have largely been capped in favor of IP networks. But in the past 12 months, bandwidth pricing for best effort IP services has declined 33% at the retail level and as much as 66% in the wholesale market.

This downward pricing trend is accelerating because of a lack of IP service differentiation and increasing competition. It is evident that service providers are struggling with a flawed business model.

Today, IP convergence occurs over MPLS platforms with the expectation of providing both best effort and premium traffic. MPLS enables circuit emulation through label-switched paths. Alone, however, MPLS is not adequate for premium services such as voice over IP (VoIP) and video, because while it supports router functionality such as “relative class of service,” it does not have the inherent mechanisms required for enforcing quality of service (QoS) guarantees.

Relative class of service refers to the ability of the router to classify packets based on the differentiated services code point in the IP header or the 3-bit EXP field in the MPLS header. While this classification enables the router to treat high-priority packets preferentially compared to best effort data traffic, it does not guarantee absolute latency and jitter bounds. For example, if a real time application mandates a per-node latency budget of 2 msec (absolute value), then the absolute latency bound required by the real time application is not supported by the router. A router that implements relative class of service can support a maximum latency of 25 msec for high-priority traffic and 250 msec for best effort traffic.

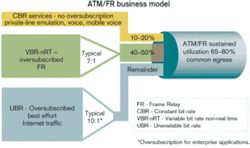

To prevent performance degradation, the average sustained use of IP/MPLS networks is kept low at typically less than 20-30%. To add to the challenges, carriers can integrate only very small percentages (typically in the single digits) of profitable premium traffic in the presence of a large amount of best effort Internet traffic, even with MPLS, further handicapping their economic model.

As a result, service providers typically use overlay networks for premium services to preserve service-level agreements (SLAs), resulting in high capital expenditures (capex) and operational expenditures. The economic issues associated with this business model are further exacerbated when investments in redundancy, stocking, and sparing are considered.

Change is needed and attention is again focused on the ATM and FR service models, which proved highly successful. ATM was developed as a Layer 2 virtual-circuit technology with QoS as an inherent design component. ATM SLAs typically support point-to-point connections with little latency, jitter, and virtually no packet loss. That enables carriers to guarantee a committed information rate per virtual circuit and charge a premium for that circuit in the presence of best effort traffic. It also allows ATM networks to operate at 60-80% bandwidth utilization levels, generating higher revenues for service providers.

Next generation IP/MPLS networks, on the other hand, specify latency and jitter in SLAs as “worst case monthly average across all city pairs.” Worst case monthly average is not a terribly useful number because latency values during highly congested durations are averaged with those during extremely light traffic. Furthermore, high latency and jitter numbers on busy circuits are averaged with those on lightly loaded circuits, for instance, New York/Los Angeles circuits are in the same pool as Providence/Hartford. As a result, the adverse impact of sub- optimum performance is not completely reflected in the SLA values. The SLAs are not violated even though the customer’s applications may suffer from sluggish performance.

IP networks are under-subscribed because of an inherent technical inability to support premium services in the presence of oversubscribed background data traffic. Incumbent router architecture, conceived in the late 1990s, was optimized to support best effort IP traffic. This earlier generation of routing equipment is unable to provide the low latency, jitter, and packet loss associated with ATM/FR equipment.

ATM backbone switches successfully combine multiple classes of premium and best effort traffic on a single converged backbone. These networks support the ability to carve out bandwidth at will for each service with bandwidth assignment enforced by the switch hardware. The ability of ATM networks to support a range of service categories with different performance guarantees allows providers to adopt a tiered pricing strategy and charge more for those services that support deterministic and extremely small bounds for latency, jitter, and packet loss.

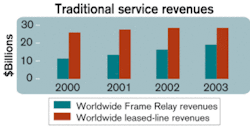

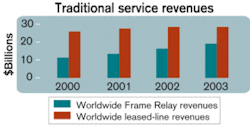

Premium services such as FR and ATM constant bit rate (CBR) have sustained much better pricing levels over the years compared to the steep decline in best effort IP pricing. A typical frame circuit is priced roughly three times more than the best effort packet service. ATM CBR is priced about four times more than a best effort IP service. The economics of ATM/FR networks are further enhanced due to the oversubscription of FR services.

For these reasons, traditional ATM and FR services have helped service providers recoup their capex in a relatively short period of time, while continuing to generate a decent profit. By contrast, carriers investing in IP/MPLS networks are having a difficult time recouping capex. This situation is not likely to change if present trends continue.

Carriers over-provisioned on IP/MPLS networks are struggling to generate profits for sustained business growth, customer and shareholder interest, and market value. Assessing the concern and growing industry challenge is the first step in arriving at a solution for overcoming the flawed economics of IP for the promise of an ATM/ FR business model.

ATM-grade IP convergence follows the proven ATM/FR business model to bring much needed profitability. It allows the efficiency of existing networks to be significantly increased with converged services, while simultaneously providing compelling service differentiation. As a result, carriers can compete on economic efficiency and superior SLAs rather than solely on price.

ATM-grade SLAs for premium IP services require service providers to specify point-to-point worst case latency/jitter bounds and packet loss metrics that surpass even those of ATM services. From a network-architecture perspective, that requires IP routers to guarantee worst case latency and jitter bounds on a per-node basis for premium traffic in the presence of background best effort data traffic. In addition, IP routers have to guarantee bandwidth for each premium application on an end-to-end basis.

ATM-grade IP convergence also requires support for multiple classes of service, each with its own distinct performance requirements. That can only be achieved if the IP routers have the ability to carve bandwidth “at will” among the multiple service classes and can guarantee that one service class does not adversely impact the performance of the other service classes. This functionality is especially important to ensure that oversubscription in certain service classes-for example, IP virtual private networks-does not adversely impact the performance of CBR-like services such as virtual leased lines, VoIP, and broadcast-quality video. The flexibility to successfully transport up to 90% premium traffic in the presence of background best effort data traffic is key to realizing a successful business model.Mukesh Chatter is president and chief executive of Axiowave Networks (Marlborough, MA). He can be reached at [email protected].