Why MSOs should be deploying all-fiber access networks

By Mark Conner

Overview

Enhancements to existing hybrid fiber/coax networks, such as DOCSIS 3.0, are providing needed capacity boosts. However, all-fiber access networks, particularly in new builds, offer high performance, economy, and flexibility in a single solution.

New technologies and changing consumer behaviors continue to require increased bandwidth capacity from access networks. At

the same time, triple-play choices, available from multiple providers, have matured and permanently changed the competitive communications landscape. Telcos continue to accelerate adoption and marketing of fiber-to-the-home (FTTH) networks, with higher bandwidth potential than the upgrades being deployed by multiple systems operators (MSOs). Not only can all-fiber access support highly competitive services but it can help control costs as well.

This article summarizes the competitive environment and the case for all-fiber access in new-build and upgrade scenarios, discusses enabling technologies, and suggests ways to incorporate all-fiber approaches into the MSO business model.

Competitive environment

Much has been written—and speculated—about the future need for bandwidth for both residential and small/medium business services. Bandwidth-intensive applications, such as streaming video and video conferencing, are an increasing share of subscribers’ bandwidth usage, which will continue to increase bandwidth demand and favor service platforms that can keep pace.1

Perhaps just as important as bandwidth demand is the breadth of competition from service providers that can offer voice, video, and data services. These providers include cable operators, phone companies, and a growing number of satellite operators with bundling partners. As video and high-speed data penetration matures, emphasis shifts to direct competition for the same customers, rather than creating new ones. This may require operators to adapt to greater variability in expected take rates. Video penetration, which changed from 58% in September of 2007 to 51% as of March 2009 according to the National Cable & Telecommunications Association, seems to reflect this. The new challenge to cable operators is thus to build their networks cost-effectively for what may be a wider range of take rates, while being positioned to provide service to all potential subscribers.

Current deployment methods using hybrid fiber/coax (HFC) technology are generally an “upfront build”—meaning that the network components (nodes, cable, amps, taps) are deployed on day one. Because of the tapped nature of the network, it is difficult to delay component deployment until service is required.

What is an AFAN?

An AFAN can service residential and/or commercial customers, including wireless backhaul, and it may be all-passive between headend/hub and the subscriber or have an active device. It is a universal platform with one overriding theme: The fiber reaches all the way to the customer premises.

In most cases, an AFAN uses optical splitting to share bandwidth (and electro-optics) among subscribers but can leverage WDM too. As a universal platform, construction for residential and commercial services uses more or less the same design and engineering principles. Most importantly, it can support a variety of transport technologies, including RF over glass (RFoG), GPON, GEPON, and soon, emerging 10-Gbps versions of GPON and GEPON without a change to the outside plant.

Interest in prestandard RFoG products is twofold. First, RFoG gets fiber in the ground now and uses the same supporting systems as HFC. Second, with fiber in the ground, enhancements through electronics overlays and migration to PONs as needed are possible for higher capacity.

Figure 1 illustrates the range of capabilities of an all-fiber network and shows the use of preconnectorized assemblies as one way to deploy that network.

Why AFANs are important to MSOs

The coaxial part of the HFC network on the subscriber side of the node is very “full.” Incremental technologies will offer increased capacity for some time, just as DOCSIS 3.0 is doing now. But even these technologies have consequences; each additional channel used for DOCSIS 3.0 means 10 standard-definition or two high-definition video channels (MPEG-2) that must be given up.4 The upstream remains an issue in HFC unless the RF mid-split is changed, or another solution is found to support more return capacity.

It is clearly understood that where viable HFC infrastructure is in place, MSOs will extend its use with upgrades such as DOCSIS 3.0 and node splitting. However, where new plant is being built, AFAN offers a platform that can support high bandwidth now and is easily adaptable to orders-of-magnitude level increases without changes to the outside plant.

Using technologies now available, such as RFoG, cable operators can push the optical signal to the home/business, instead of stopping at the node. When added capacity is needed, operators can implement a wavelength overlay or equipment change. Several equipment vendors now support the addition of EPON or GPON overlays to add capacity to the network on an individual subscriber or system basis.

Distributed splitting, in which the 1×32 is broken into layers, reduces distribution fiber counts and cabling costs but may also reduce subscriber management and flexibility. Still, distributed splitting can be a valuable enabler, especially in medium-, low-, and rural-density applications. For both architectures, thoughtful inclusion of spare fibers provides adaptability, especially where land development is less predictable.

How can an MSO leverage AFANs?

An AFAN approach offers the greatest promise today for new builds and extensive rebuilds. These locations would therefore be the best candidates for initial deployments of new AFAN systems.

Using a preconnectorized cable, the “backbone” can be installed while the terminals for drop connection are deferred until needed. The initial installation costs include material and labor for the splitter housing, splitters for a portion of the potential subscribers, and the distribution cable assemblies to pass all prospective subscribers. All splicing is performed at the initial installation, and all subsequent components are added by plugging them in using multifiber and single-fiber hardened connectors. Thus, expensive splicing labor is used efficiently and incremental adds do not require special skills or equipment.

Because a preconnectorized AFAN is ready for terminals to be plugged in, it can be put in when the neighborhood is very close to generating service requests. For example, conduit can be placed during joint trench opportunities and the assembly placed much later, avoiding potential hazards from ongoing construction.

A sample design can illustrate the AFAN approach relative to HFC. The design parameters include:

- typical suburban neighborhood density with 700 to 800 homes passed

- cable plant is in duct for both AFAN and HFC

- pedestals are used for AFAN terminals and HFC taps

- all AFAN terminals are deferred from the initial build

- AFAN terminals are added at twice the take rate—at 15% take rate, 30% of the terminals are installed; at 50% take rate, all terminals are installed

- HFC is built out completely upfront (all coaxial cable, taps, nodes, amps, etc.)

- the AFAN subscriber connection includes headend electronics (scaled), a drop assembly, optical network unit (ONU), and placement costs

- the HFC subscriber connection includes drop, house splitter, and placement

- neither system has modems, voice equipment, or set-top boxes

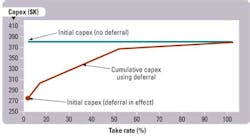

Figure 3 illustrates the deferral opportunity enabled with preconnectorized AFAN assemblies. The beginning of the red curve is the initial capex requirement when deferral is used. The red curve then describes the cumulative capex (initial capex plus incremental terminals and splitters) as take rate rises.

The green line indicates capex when deferral is not used. In this case, all terminals and splitters are installed upfront; the full cost is borne when the take rate is zero. Note that the red line only reaches the full capex (green) line if a take rate of 100% is achieved. In this sample design, about 27% of the material and labor has been deferred.

By adding the initial and incremental passive costs to the subscriber connection costs (remember, HFC is an all-upfront build, except for the drop), it is possible to plot the cost per home connected (subscriber) as take rate increases. Figure 4 shows that AFAN is potentially less expensive than HFC until parity is reached at a take rate of approximately 50%. Current cable industry take rate for video is reported at 51%.

Capacity today and tomorrow

The broadband services market continues to evolve, with the potential for a wider range of observed take rates due to competition. In this environment, attention to capex increases with the objective of building a “modular” network that can be deployed and adapted as take rates require.

An AFAN approach enables part of the initial capex to be deferred with easy, “no-splice” installation of components when needed. In the example shown, one-fourth of the passive costs could be deferred, with AFAN/HFC cost parity occurring at about a 50% take rate. Of course, results will vary according to such parameters as density and the sophistication of the electronics used.

Beyond just deploying a fiber architecture, an AFAN creates a platform upon which both current and future technologies can provide order-of-magnitude level increases in capacity when needed. An AFAN also offers up to an 80% reduction in maintenance costs and promises cost reduction through fewer power supplies or even none at all. An AFAN gets “fiber in the ground” cost-effectively today and offers the long-term bandwidth capacity needed for competition in an evolving market environment.

References

- 1. Morgan Stanley Report, “Cable/Sat & Telecom,” April 17, 2009.

- 2. S. Eleniak, “The Rationale for RFoG,” Converge! Network Digest, May 5, 2008 (http://www.convergedigest.com/bp/bp1.asp?ID=529&ctgy=).

- 3. G. Kim, “BT Sees Opex Opportunity,” IP Business News, July 25, 2008 (www.ipbusinessmag.com).

- 4. “DOCSIS 3.0 vs. FTTH: An Exploration (Panel Discussion),” The FTTH Prism, Vol. 5, No. 3, June 2008.

- 5. D. Russell, “GPON Deployments by Cable Operators,” CEDMagazine.com, Oct. 1, 2008.

Mark Conner is a market development manager, Corning Cable Systems (www.corningcablesystems.com).

Links to more information

LIGHTWAVE ONLINE:HeavyReading: Cable Operators Turning to Fiber

LIGHTWAVE:Consultant: PON Best Bet for MSOs

LIGHTWAVE:MSOs Want Their FTTH and DOCSIS, Too