In a recent 12-month period, telecommunications competitors extended their fiber-network

In a recent 12-month period, telecommunications competitors extended their fiber-network route-miles by 125%.

Richard G. Tomlinson

Connecticut Research

Competition in the local telecommunications market underwent significant changes in 1994 that accelerated the deployment of fiber-based metropolitan area networks. Although many analysts assert that the United States is "over-fibered" with a glut of redundant networks, telecommunications market ventures prove otherwise. Market studies disclose that competitors are spending increasingly large amounts of capital to achieve adequate connectivity with their customers.

Fiber deployment by traditional service providers and their competitors is expected to continue increasing for several years while the regulatory, technological and market structures of the United States telecommunications industry markedly change. The industry is predicted to move to a system of multiple, competing local telecommunications service providers with independent, but interconnected, networks.

Expanded service offerings

In addition, bifurcated local and long-distance services are projected to evolve into integrated local, long-distance and international services offered by competing consortiums of service providers.

High-bandwidth transport should eventually become a ubiquitous commodity. But for now, fiber deployment advances intensely as a growing number of service providers position their products to serve the local telecommunications market.

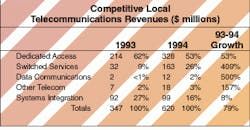

Companies engaged in the competitive local telecommunications market have previously been referred to as competitive access providers or CAPs. The name has been appropriate because the bulk of their revenues was derived from providing transport for dedicated access to long-distance carriers.

In 1994, dedicated access accounted for more than half of the competitive local telecommunications industry revenues, but other revenue sources were growing faster. In 1995, revenues from switched services are predicted to become the leading source of industry revenues. This transition should occur even though only a few states permit full-scale competition for local telephone service. Switched services include switched access, long-distance toll, local dial-tone and associated services.

In 1995, revenues from switched services should exceed those from dedicated access. Switched services should continue to boost revenue growth for the competitive industry. By 1999, total industry revenues should exceed $10 billion, with more than 70% of the revenues coming from switched services.

These changes in the competitive local telecommunications business should be reflected in network architecture changes. Networks should evolve from simple rings and trunks into complex mesh structures, such as interconnected "network-of-networks" environments. Multiple technologies, including wireless, are planned to achieve "end-loop" connectivity to end users.

Networks will incorporate distributed switching with remote switching modules on fiber that is "homed" on central office switches hundreds of miles away.

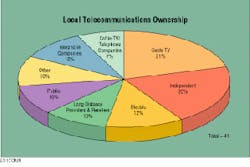

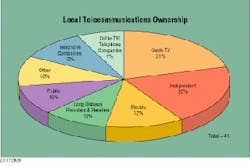

Many new providers entered into the local competition in 1994, including long-distance carriers, electric power companies and out-of-region telephone companies. As a result, cable-TV companies became less dominant in terms of ownership of the companies involved in local telecommunications competition.

In 1994, cable-TV companies represented the largest single ownership bloc. More than 20% of the competitive companies are wholly owned by cable-TV companies and another 7% are jointly held by cable/telephone company partnerships.

In contrast, only 12 months earlier, more than 50% of the companies involved in local competition were cable-TV owned. The dramatic downturn was not a result of market withdrawal by cable-TV companies but the entry of many diverse players.

Entrepreneurial companies, for example, are now the second largest ownership group, representing 20% of the total, whereas telephone companies, electric utilities, long-distance resellers and public telephone companies each represent 10% of the industry. The direct entry of long-distance carriers into local competition is expected to significantly affect the installation of metropolitan area networks.

Note that the listing of competitive networks does not include MCI Metro, which MCI Communications Corp. created last year to enter the competitive access business. MCI Metro has been slow to ramp up, but has acquired right-of-way, conduit and fiber assets from Western Union. These assets should permit rapid network growth to more than 3000 route-miles of fiber MANs in 20 major cities.

Sprint, in combination with the cable-TV owners of the Teleport Communications Group, is expected to stimulate MAN fiber deployment as the long-distance carrier moves toward integrated local and long-distance services.

Traditional local telephone companies, such as US West with Time Warner Communications and Century Telephone with Metro Access Networks, have also begun to enter competitive telecommunications areas outside their franchise territory.

Changing demographics

Early builders of competitive fiber MANs linked buildings clustered in the central business districts to the nearby switching centers of long-distance carriers. Consequently, the density of buildings on the network (buildings/mile) was relatively high. As these networks have matured, they have been extended to outlying industrial parks and suburban locations. Accordingly, network route-miles rapidly have increased.

Study results show a progressive decline in the density of buildings-on-net. The average network density declined from 0.95 buildings per mile in 1992 to 0.75 buildings per mile in 1993, and to 0.68 buildings per mile in 1994.

This density decrease is expected to continue as more networks grow regional rather than urban in extent, as networks are developed in smaller cities and as electric utility and cable systems are used to install fiber. The trend will probably not reverse unless cable-based fiber systems begin to serve significant numbers of residential telecommunications customers.

Study results also indicate that more than 83 metropolitan statistical areas have competitive fiber MANs. Not to be outdone, network construction in smaller markets is more feasible because of the combination of declining fiber network construction costs and the increasing revenue potential from expanded service offerings. Competitors were initially limited to offering dedicated, high-bandwidth transport. Such services are primarily used by large corporations and long-distance carriers. As regulatory changes permit competition for more telecommunications services, particularly switched services, competitive networks are able to serve small and medium-sized businesses and, eventually, residential customers.

Competitors of local telephone companies dramatically accelerated their deployment of metropolitan area networks in 1994. During the 12-month period from July 1993 to July 1994, MAN route-miles increased 125%, from 5190 to 11,693. This sharp upturn occurred because competition grew in network size, geographical presence, market penetration, capital investment, service offerings and revenues.

Led by Teleport Communications Group Inc. and MFS Communications Co. with 2813 and 1783 route-miles, respectively, more than 40 companies are engaged in network-based competition. In fact, 22 companies have more than 100 miles of fibered networks in service.

This surge in activity contrasts with the previous 12 months when the number of competitive companies declined under a wave of consolidations and mergers, and total network growth barely exceeded 40%. A major source of the acceleration in network growth was the aggressive deployment of fiber for telecommunications by cable-TV system operators. Because many ambitious new projects are pending, this trend shows no sign of slowing.

Although primarily fiber-based, the total network route-miles in 1994 include 1172 miles of digital microwave, as well as 10,521 miles of fiber. Not all the growth in fiber route-miles represents new construction between July 1993 to July 1994. Particularly in networks built by cable-TV companies, some fiber was deployed earlier and only recently identified as delivering telecommunications services. Nevertheless, new fiber mileage more than doubled during the period.

Teleport Communications Group was the leading company in total deployed network route-miles during July 1993 to July 1994. Through joint venture projects with cable-TV companies, this competitive access provider has maintained rapid growth in route-miles for its fiber network. In fact, it is owned by four of the largest U.S. cable-TV operators -Tele-Communications Inc., Cox Enterprises Inc., Comcast Corp. and Continental Cablevision, Inc. In 1993, Teleport formed TCG Affiliate Services to promote more rigorously joint ventures with cable-TV companies.

In June 1994, TCG announced the formation of joint ventures with 11 large cable-TV operators, for building new networks and expanding existing networks. This program has since been expanded. Each joint venture is separately formed to develop a specific market.

In each venture, one or more of the local cable-TV companies constructs and maintains the fiber network and TCG conducts a telecommunications business over the network. Revenues are shared based on an agreed formula for the local market`s "propensity to consume telecommunications services."

Network capacity

Because route-miles are a measure of network reach, the latent capacity of fiber networks is a function of the effective cable cross-section. This capacity is often expressed in terms of fiber-miles, or the product cable sheath miles times the average number of fibers in the cross-section. Study results imply that networks in the United States totaled 392,339 fiber-miles in July 1994, for an effective average cross-section of 37 fibers.

However, this data is only an indicator of latent capacity because many fibers are initially installed for future expansion. These dark fibers are not connected to active electronics. Typical metropolitan area networks in service today are projected to contain from 50% to 90% dark fibers.

Richard G. Tomlinson is president of Connecticut Research in Glastonbury, CT.