Third quarter 2017 follows year-long theme for optical communications: LightCounting

LightCounting states in its newly released "December 2017 Quarterly Market Update" that demand for optical communications technology in the third quarter of 2017 followed what has so far been a year-long trend: Service provider spending declined year-on-year while data center operators increased their investments.

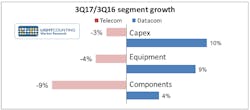

As illustrated in the graph above, the decline in spending among telecom companies hit the optical components segment hardest, but was unkind across the board. Chinese carriers followed through on their announced plans to trim spending. Perhaps ominously, LightCounting reports that China Telecom will continue to cut capex in 2018. Elsewhere in the world, only Orange looks like it will spend more this year than last among LightCounting's list of top 15 telecom service providers.

Optical technology vendors looking for rays of light within the service provider gloom found them in sequential growth 100G DWDM transponders and WSS module sales. However, these upticks paled in comparison to the declines experienced in the FTTx and wireless fronthaul markets, both sequentially and annually (see "Demand for FTTx, wireless optics declines from 2016: LightCounting"). That said, LightCounting reports that check-ins with semiconductor vendors such as Analog Devices, Qualcomm, and Xilinx revealed increased activity in wireless communications, including 4.5G and 5G projects. This information leads the market research firm to expect initial commercial deployments of next generation wireless technologies in 2018, which in turn should boost the demand for optical fronthaul technology.

The news overall was much better for technology vendors with exposure to the data center and internet content provider markets. Alibaba, Facebook, and Google increased their infrastructure spends by 142%, 62% and 39%, respectively, leading to overall spending records in the space during the quarter. Facebook, meanwhile, plans to double capex in 2018 according to LightCounting, leading to hopes the growth is sustainable. Optical transceiver vendors benefited from the operators' largesse during the quarter, which Applied Optoelectronics seeing a 27% increase in revenuesandInnolighta 94% boom versus 3Q16. Shipments of PSM4 and CWDM4 100GbE modules set records during the quarter. However, 100GBASE-LR4 QSFP28 optical transceiver demand in the third quarter of 2017 proved softer than LightCounting expected.

For related articles, visit the Business Topic Center.

For more information on optical modules and suppliers, visit the Lightwave Buyer's Guide.

About the Author

Stephen Hardy

Editorial Director and Associate Publisher

Stephen Hardy has covered fiber optics for more than 15 years, and communications and technology for more than 30 years. He is responsible for establishing and executing Lightwave's editorial strategy across its digital magazine, website, newsletters, research and other information products. He has won multiple awards for his writing.

Contact Stephen to discuss:

- Contributing editorial material to the Web site or digital magazine

- The direction of a digital magazine issue, staff-written article, or event

- Lightwave editorial attendance at industry events

- Arranging a visit to Lightwave's offices

- Coverage of announcements

- General questions of an editorial nature

Voices of the Industry