Cloud and Data Center Interconnect (DCI) creates a new coherent optics wave

Key Highlights

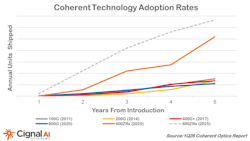

- Interest in ZR+ optics is rising sharply, with a tenfold increase over the past year, driven by the need to connect larger AI data centers over longer distances.

- The market for IPoDWDM systems is expected to grow nearly 40% in 2025, with shipments of ZR+ modules increasing significantly in 2026 to support hyperscale data center expansion.

- Cignal AI and Dell’Oro forecast that over 25% of IPoDWDM revenue will come from non-DCI applications by 2030, reflecting broader adoption across communication service providers.

- Leading vendors like Marvell, Cisco, and Ciena are focusing on interoperability and long-distance capabilities, with new product launches supporting 800G and 1.6T connections for AI workloads.

- The shift towards pluggable coherent optics is making embedded optics increasingly reserved for ultra-long-haul and subsea routes, emphasizing operational flexibility and performance improvements.

Driven by the scale of data center buildouts for AI training and aggressive cloud upgrades, interest in and deployment of ZR+ optics continue to rise.

Industry analyst reports from Dell’Oro and Cignal AI are forecasting strong growth in coherent optics.

Dell’Oro Group’s latest IPoDWDM and Disaggregated WDM report revealed that IPoDWDM systems demand is expected to grow at an average annual rate of 16 percent, reaching $4.4 billion by 2030.

The research group also found that shipments of ZR+ optical pluggable modules for routers and switches are expected to increase in 2026 as hyperscalers scale across data centers to build larger AI factories.

Following the recovery in the second quarter of 2024, Dell’Oro forecasts that the IPoDWDM market will grow nearly 40 percent in 2025. ZR optics is the dominant pluggable used in IPoDWDM to date.

While DCI is a key driver, traditional service providers’ interest in IPoDWDM is rising.

Dell’Oro said that “over 25 percent of IPoDWDM system revenue is expected to be from non-DCI applications by 2030 as more communication service providers adopt the technology in their networks.”

Likewise, Cignal AI’s new Coherent Pluggable Optics Active Insight report, found that coherent pluggables now lead in deployed bandwidth, overall market size, and bandwidth growth, with 400ZR/ZR+ firmly established and 800ZR/ZR+ beginning large-scale rollouts this year in support of AI scale-across architectures.

Looking forward, the research firm expects that future 1600ZR technology will extend pluggable leadership, while the use of traditional embedded optics becomes increasingly confined to the most demanding deployments – subsea and ultra-long-haul routes – where their performance advantages still justify higher cost and power.

“Coherent networking has become a pluggable world,” said Scott Wilkinson, Lead Analyst at Cignal AI. “The economics, operational flexibility, and rapidly improving performance of pluggables dictate that embedded coherent optics will be the exception rather than the rule – reserved for only the hardest routes in the network.”

800ZR+ rising

The 800 ZR+ is set for greater growth in the coming year.

Driven by scale across DCI, Dell’Oro said 800 ZR+ optical module shipments will drive a “sharp increase” in 2026. Also, the research firm noted that over one-third of IPoDWDM ZR/ZR+ revenue is expected to be from 800 ZR/ZR+ module shipments in the year.

Scale-across DCI is expected to change the market dynamics, driving a sharp increase in 800 ZR+ optical module shipments in 2026. Based on projections for volume and average sales price, over one-third of IPoDWDM ZR/ZR+ revenue is expected to be from 800 ZR/ZR+ module shipments in the year.

“The interest level in ZR+ optics has grown by ten times since just a year ago,” said Jimmy Yu, Vice President at Dell’Oro Group. “In the original inception of coherent ZR pluggable modules, the dominant use case was for interconnecting data centers less than 80 kilometers apart. The ZR+ versions were developed as an afterthought, with no clear need. Since then, with the sudden rise in power-hungry AI data centers, the need has shifted to moving data centers farther out, with much more fiber capacity between them to handle the intensive AI workloads.”

He added that “the need to scale across data centers to build up AI training centers is sharply pivoting demand for IPoDWDM systems with large amounts of ZR+ optics.”

Cignal AI’s Wilkinson agreed.

“400ZRx is now the most widely adopted coherent technology to date, and 800ZRx is on track to surpass it as hyperscalers deploy higher speeds to support DCI and AI."

Marvell, Cisco and Ciena dominate

Marvell, Cisco, and Ciena were the three dominant players in the ZR/ZR+ optical pluggable modules market by shipment volume.

Marvell, Cisco and Ciena dominate and Ciena were the three dominant players in the ZR/ZR+ optical pluggable modules market by shipment volume.

Driven by the AI boom and hyperscaler demand to scale data centers, Marvell’s ZR+ pluggable optics are experiencing ongoing growth. The company expects shipments to ramp in 2026 as they enable long-distance, high-bandwidth connections (800G/1.6T) directly into switches.

Interoperability is a key focus for Marvell. In September 20024, Marvell Technology, Lumentum Holdings Inc., and Coherent Corp. conducted an interoperability demonstration of 800G ZR/ZR+ optical modules over transmission links up to 500km.

Cisco is also seeing growing interest in its ZR+ platforms. The company’s 800G ZR+ coherent optics have been tested in live network field trials by major carriers such as Arelion, demonstrating significant operational expenditure (OpEx) savings (up to 95%) and long-distance capacity increases (e.g., 1,069 km).

Like Marvell and Cisco, Ciena also expects interconnects to play a meaningful role in scale-up, scale-out, and scale-across networks.

Ciena reported that in fiscal year 2025, it surpassed its target of more than doubling FY24 pluggable revenue, reaching $168 million. “In the quarter, our WaveLogic 6 Nano 800-gig pluggables were shipped for initial revenue,” said Gary Smith, CEO of Ciena. “And since the end of the quarter, we have shipped 800 ZR plugs to three additional cloud providers for testing and certification.”

But coherent optics is not just about data centers.

Other vendors, such as Ribbon, are also making progress with IPoDWDM. Ribbon is expanding its IPoDWDM platform customer base in the U.S., particularly among rural providers expanding their fiber-to-the-home (FTTH) networks.

“We expect these deployments to accelerate meaningfully in 2026 with federal funding,” said Bruce McLelland, CEO of Ribbon, during the company's fourth quarter earnings call.

For related articles, visit the Optical Tech Topic Center.

For more information on high-speed transmission systems and suppliers, visit the Lightwave Buyer’s Guide.

To stay abreast of fiber network deployments, subscribe to Lightwave’s Service Providers and Datacom/Data Center newsletters.

GenAI boosts enterprise cloud revenues to $119B

Synergy Research’s latest market report found that fourth-quarter enterprise spending on cloud infrastructure services jumped by almost $12 billion from the previous quarter and by $29 billion from the fourth quarter of 2024. The research firm said the “scale of these increments far surpasses anything previously seen in this market,” adding that the 2025 full-year market reached $419 billion. With 30% growth from the fourth quarter of 2024, this marks the ninth consecutive quarter of accelerating year-on-year growth and the highest growth rate the market has seen in more than three years.

About the Author

Sean Buckley

Sean is responsible for establishing and executing the editorial strategy of Lightwave across its website, email newsletters, events, and other information products.

Voices of the Industry