Carrier choices will define wireless backhaul opportunity

By Stephen Hardy

Much like the wireline space, wireless networks may require something of an overhaul to efficiently support the delivery of voice, video, and data services to a rapidly growing customer base. Again as in the wired market, several system suppliers believe this revamping will lead to more fiber in wireless backhaul networks, perhaps even greater instances of cell towers directly connected with fiber. However, anyone ready to coin a new “fiber to the” acronym should be aware that wireless network operators have a variety of options at their disposal when it comes to evolving their infrastructures to meet changing requirements.

Most cell sites, particularly those in North America and Europe, use T1/E1 links to backhaul traffic from cell towers and Node B cell sites to aggregation points that usually connect to SONET/SDH networks (digital microwave links make up most of the unwired connections). This arrangement has become increasingly unsatisfactory for three reasons.

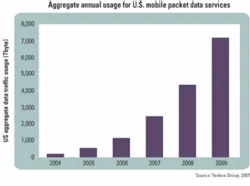

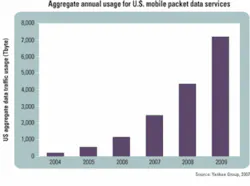

Growing bandwidth requirements represents the first. Even without the advent of triple-play service offerings, the sheer number of mobile users would have put the squeeze on current backhaul strategies. Infonetics Research (www.infonetics.com) estimates that there were more than 2 billion mobile subscribers worldwide in 2005; they expect that number to increase at least 50% by 2009. Add the increasing bandwidth demands of individual services powered by 3G wireless technology, particularly data for both business and individual consumers as well as video, and a single T1/E1 line per cell tower quickly becomes insufficient.

The wider variety of services poses the second problem, particularly when it comes to providing traditional services that are based on ATM and TDM today with an eye toward Ethernet and IP tomorrow. Carriers face the dilemma of whether to run separate backhaul networks for voice and data or combine the two into a single infrastructure-which would mean either settling on a single transmission protocol or connecting the link to a platform, such as a multiservice provisioning platform (MSPP) or a pseudowire-enabled system, that can handle multiple protocols simultaneously.

The final problem is cost. Backhaul is extremely expensive. Yankee Group (www.yankeegroup.com) estimates that backhaul takes up an average of 10% of a carrier’s opex worldwide. However, the research firm believes that number rises to 35% in the U.S. market, where wireless operators can expect to pay around $600 per T1. As Vince Vittore, a Yankee Group senior analyst, wrote in a recent report, “Using multiple T1s for backhaul, however, provides no volume discount for wireless carriers. It simply adds cost.”

Added together, carriers spent $16 billion on wireless backhaul in 2005 and will spend twice that in 2009, according to Infonetics Research. With numbers like that, it’s no wonder that an increasing number of optical systems vendors have identified wireless backhaul as a potentially lucrative opportunity. However, there appears to be disagreement about where the opportunity actually resides and who is in the best position to benefit.

Analysts appear to agree that optical technology will be the clear winner in aggregation networks. The question will be what kind of platforms will form the hubs; the answer to that question will come as carriers decide how they want to handle packet-based traffic.

As stated before, most wireless operators are looking at MSPPs, Ethernet routers, and IP platforms to handle digital services on a converged network-or just running two networks for the time being. Whatever the choice, optical vendors should benefit, analysts believe.

“There is clearly going to be a demarcation of the TDM-based voice (2G) traffic and ATM- or IP-based data (3G) traffic in the backhaul, and so we might see a hybrid approach in the near and medium term trying to carry voice and data over different networks and thus the need for aggregation boxes that combine different traffic flows,” suggests Aditya Kaul, who is currently working on a wireless backhaul report for Pioneer Consulting (www.pioneerconsulting.com). “The presence of MSPP aggregation boxes is another area where we could see a role for optical companies. In general, aggregation boxes are moving closer to the base station, shortening the route where microwave or T1/E1 access traffic flows, thus allowing for optical components to have a stronger footprint.”

Nick Maynard, another analyst at Yankee Group, agrees that the aggregation network is where the optical opportunity begins, shaped by the quandary of how to handle packets. “Optical agg (whether that’s Ethernet, PBT, T-MPLS) makes a lot of sense,” he wrote in an e-mail response to questions. “The issue with PBT is the [point-to-point] limitations that might be a problem as mobile carriers feed more services to their customers and need to access different video or application servers across the network.”

Kaul likes MPLS in the long term. “There are multiple approaches being suggested, especially in the aggregation layer of the backhaul network, but in general we see the IP/MPLS core network being pushed closer to the aggregation and access layers of the backhaul network,” he writes via e-mail. “We have seen this solution being suggested by many operators here in Europe who have IP/MPLS core networks. This is certainly one area where optical companies could play a bigger role.”

Infonetics agrees that the market will favor IP/MPLS, with an emphasis on pseudowire technology. The company forecasts that IP mobile backhaul equipment will represent 45% of sales ($1.1 billion) by 2009; of this equipment, 99% will be pseudowire enabled.

However, pure-play Ethernet also may find a home. This is certainly the hope of companies such as World Wide Packets (www.worldwidepackets.com), which recently unveiled a Carrier Ethernet aggregation platform, the LE-3300, that the company expects will play in wireless backhaul applications. Mike Nielsen, executive vice president, and Chad Whalen, senior vice president, global sales and marketing for World Wide Packets, say that Ethernet and PBT offer advantages over IP/MPLS for wireless backhaul. Ethernet routers are less expensive than their IP counterparts and provide less complexity, they say; meanwhile, PBT may provide superior quality of service-and certainly quality-of-service mechanisms closer in operation to the SONET/SDH schemes carriers are used to-due to an ability to handle the vagaries of wireless data streams that could be superior to IP/MPLS. The company executives also say that PBT-based management could leverage an optical infrastructure’s existing operational support system. Only the endpoints of the network would need to be “PBT aware”; the infrastructure in between could be based on Ethernet.

The choice of transport protocol will also affect how close fiber comes to the individual cell tower. A move toward native Ethernet generally would be beneficial to optical proponents-although an embrace of Ethernet wouldn’t necessarily mean fiber to the tower would become the norm. As Yankee Group’s Vittore pointed out in the aforementioned report, Ethernet over copper technology would enable carriers to use existing infrastructure to significantly increase the pipeline T1s/E1s currently provide. Such an option should prove particularly tempting in light of the fact that Yankee Group estimates that there are 158,500 cell towers in the U.S., about 1.8 million globally-and less than 10% of them currently have a fiber connection.

Thus, carriers face the same decision with cell towers as they do when providing broadband to homes. Using a single fiber pair and the SHDSL.bis standard, Vittore says carriers theoretically can get 5.7 Mbits/sec per pair in and out of cell sites. The question is whether that will be enough to avoid making an investment in fiber.

For some sites, the answer will be yes. However, Vittore believes Ethernet over copper will remain a niche technology, limited to applications where there isn’t fiber already available, the cost of extending fiber to the site is exorbitant, the bandwidth demand at the site requires a fatter pipe, and there are enough alternative backhaul options in the market to force a telephone company to replace its revenue-generating T1/E1 services. Such alternatives may come from cable MSOs; Vittore writes that most of them will offer services using fiber.

But if one can relegate Ethernet over copper to niche status, that doesn’t mean fiber will rule the wireless world. Digital microwave links also can be used for wireless backhaul from cell sites, and proponents point to their superior performance versus wireline alternatives during the Hurricane Katrina disaster as proof of their suitability. Infonetics estimates that in 2005 microwave radios composed 81% of total mobile backhaul equipment sales worldwide and 56% of total connections.

With this in mind, most analysts expect the number of fiber-enabled cell sites to grow but not obtain dominant status. “From my interviews with the vendors and the carriers, there seems to be a slow move towards fiber for individual cell sites,” Maynard concludes. “There will be many more sites hooked up with fiber, but it will take time and there are still going to be lots of sites connected with copper that just won’t have the bandwidth requirements that make a fiber-based deployment cost-effective.”