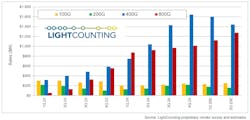

800G transceivers will be a second-quarter market growth driver

Following flat sales in the first quarter, LightCounting expects optical transceiver sales to rise 10% during the second quarter.

The research firm expects sales of 800G Ethernet transceivers to drive most of the growth.

And while it’s still early in the game, LightCounting said it expects that sales of 1.6T transceivers “will also make a modest contribution to the market in the second quarter.

However, sales of 400G Ethernet modules will drop as Amazon and Meta transition to higher-speed modules.

Meanwhile, the 400G and 800G AOC sales will also remain strong, while a rebound from a seasonally slow Q1 in sales of DWDM, FTTx, and WFH transceivers will contribute to a stronger second quarter.

But the research firm said, “No significant recovery is expected in the telecom market.”

Flat telecom growth

In the traditional telecom provider industry, first-quarter revenues were flat.

Making matters worse was that capital expenses declined 5% year-over-year from the first quarter of 2024.

LightCounting noted that the three leading Chinese telecom providers — China Mobile, China Telecom, and China Unicom—are all reducing their capital expenditures (capex) this year. The total spending of the three will be $39.8 billion in 2025, down 10% from 2024.

There were some bright spots.

Softbank led the pack with 7% growth, followed by Deutsche Telekom (up 3%) and China Unicom (up 3%), compared to the same quarter a year ago.

Alternatively, Telecom Italia’s revenues dipped 19%, while Telefonica’s revenue was down 12% year-on-year, both due to the sale of businesses focusing on strategic assets.

In the U.S., service provider dynamics are entering a period of flux on both the traditional telco and cable operator sides.

AT&T and Verizon have made deals to acquire Lumen’s consumer fiber business and Frontier. Meanwhile, Charter is acquiring Cox Communications.

Other notable M&A developments are emerging from competitive carriers, such as Zayo, which has reached a deal to acquire Crown Castle’s fiber services businesses.

“Mergers and acquisitions activity is growing, notably in the US with TSPs acquiring fiber assets and in Europe where operators are divesting and focusing on core markets,” LightCounting said.

Cloud and hyperscalers rise

Cloud and hyperscaler capital spending continues to rise, a trend that was evident amongst the largest providers in the first quarter.

LightCounting noted that Alphabet, Amazon, Meta, Microsoft, and Oracle continued to spend “significantly more in Q1 2025 than in Q1 2024.”

While Oracle is the smallest of the Top 5 providers, the company’s capital expenditure (capex) spending rose 233%, reaching $5.6 billion—more than 50% of its total spending for the year.

Alibaba reported $32.5 billion in revenue, up 5% compared to the same quarter last year but down 17% sequentially. On the capital expenditure (capex) front, Alibaba has set a plan to invest approximately $53 billion in AI infrastructure over the next three years.

Baidu reported $4.5 billion in revenue, up 3% year-over-year, down 5% sequentially. The company reported spending of $398 million, up 41% year-over-year and 23% sequentially.

Finally, Tencent reported revenue of $24.7 billion, up 12% from the same quarter a year ago and 3% above the fourth quarter of 2024. During the quarter, the company spent $3.7 billion, representing an 89% increase compared to the same period last year, but a 36% decrease sequentially.

For related articles, visit the Business Topic Center.

For more information on high-speed transmission systems and suppliers, visit the Lightwave Buyer’s Guide.

To stay abreast of fiber network deployments, subscribe to Lightwave’s Service Providers and Datacom/Data Center newsletters.