Key Highlights

- AT&T maintains its top position in the U.S. Carrier Ethernet leaderboard, driven by fiber network investments and next-gen service deployment.

- The market is stabilizing with less than 4% share difference among top players, emphasizing a mature and competitive landscape.

- Lumen is focusing on enterprise services and AI-ready networks, despite revenue challenges and strategic asset sales.

- Verizon is strengthening its managed services through partnerships like HCLTech, aiming to improve EBITDA margins and service offerings.

- Cable providers like Charter and Comcast are expanding into larger business segments, leveraging wireless partnerships and cloud services to compete with traditional telcos.

Recommended Reading

- AT&T Business serves up single-vendor SASE with Cisco

- AT&T’s CFO says Lumen deal will deepen its fiber and wireless presence

- Lumen says Trump’s AI action plan bolsters its fiber network plans

- Charter’s CEO says T-Mobile partnership opens the door for business wireless sales

- Comcast’s CEO says T-Mobile pact will enhance business market share

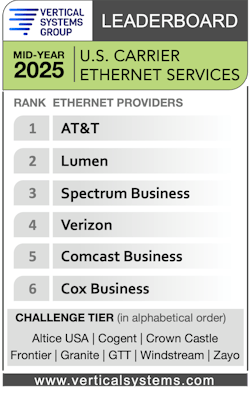

AT&T continues to hold the top ranking on Vertical Systems Group’s Mid-2025 U.S. Carrier Ethernet LEADERBOARD, reflecting its aggressive fiber network and next-gen services build-out strategy.

The service provider’s ongoing efforts resulted in a 3% reduction of its operating expenses during the second quarter, which was mainly due to lower personnel and customer support costs associated with ongoing transformation initiatives, partially offset by higher depreciation expenses resulting from ongoing investments in strategic initiatives, such as fiber.

Pascal Desroches, CFO of AT&T, said that these actions will enable it to emphasize its fiber-based service set. “We expect to reinvest some of these savings in the third quarter to drive future growth in fiber and advanced connectivity revenues,” he said.

Being an incumbent telco, AT&T is not immune to legacy revenue decline pressure from TDM-based services—a trend that continued into the second quarter. AT&T Business Wireline's operating income decreased by $201 million, compared to $102 million in the year-ago quarter.

“Business Wireline revenues declined year over year, driven by continued secular pressures on legacy and other transitional services that were partially offset by growth in fiber and advanced connectivity services,” AT&T said in its second-quarter earnings release.

Joining AT&T on the top list are Lumen, Spectrum Business, Verizon, Comcast Business, and Cox Business. Mid-year 2025 U.S. Carrier Ethernet market shares for four of the six LEADERBOARD companies are within less than 4%.

VSG said that the “U.S. Carrier Ethernet market is stable and maturing.”

Lumen and Verizon’s struggles and opportunities

Lumen and Verizon continued to see business service opportunities and struggles during the second quarter.

With the sale of its consumer in play, Lumen is set on carrying out its mission to become a business-centric service provider.

As it expands its metro and long-haul fiber networks, Lumen is focused on being able to provide network connectivity that supports AI.

A key element of Lumen’s AI strategy will be its Private Connectivity Fabric (PCF) solutions. These solutions design a custom, AI-ready network architecture.

However, in the second quarter, it saw service revenue challenges. Due to declines in VPN and Ethernet revenue, overall Business segment revenue fell 3.4% to $2.49 billion.

Despite the near-term declines, Chris Stansbury, CFO of Lumen, said the company is confident that the $5.74 billion sale of its consumer fiber business to AT&T in May is a positive step because it “allows us to invest and focus on our core enterprise capabilities while also significantly improving our balance sheet.”

Likewise, Verizon saw its share of challenges during the second quarter. The service provider reported that total Verizon Business revenue was $7.3 billion in the second quarter of 2025, down 0.3 percent year-over-year.

As seen in earlier quarters, Verizon’s business wireless service revenue in the second quarter of 2025 was $3.6 billion, an increase of 1.6 percent year-over-year. Business reported 65,000 wireless retail postpaid net additions in the second quarter of 2025.

Verizon has set the stage for potential managed services growth with its HCLTech partnership. In 2024, Verizon Business struck a partnership, making HCLTech its primary Managed Network Services (MNS) collaborator in all networking deployments for global enterprise customers. The partnership combines Verizon’s networking, solutioning, and scale with HCLTech’s Managed Service capabilities.

“The deal we signed with HCL is providing a lot of benefits this year and a lot of good discipline in terms of moving customers off of legacy products and deemphasizing low-margin deals and also operating with lower headcount,” said Hans Vestberg, CEO of Verizon, during its second-quarter earnings call. “So, we're well-positioned to continue to improve the business EBITDA margins this year. We're very happy with the progress.”

Cable shifts

In the cable market, Tier 1 providers are making moves that will enable them to challenge traditional telcos on the Ethernet and advanced services front.

The two largest cable operators—Charter and Comcast—continue to expand from their small to medium business (SMB) roots to providing Ethernet and advanced cloud services to larger businesses.

Charter, which is in the process of merging with Cox Communications, reported that second-quarter commercial revenue grew by 0.8% year-over-year due to a boost in the mid-market and large business segments. However, small business revenue declined by 0.6%, reflecting a decline in small business customers with revenue per customer remaining essentially flat year-over-year.

But the big shift for Charter will be in being able to deepen its wireless presence with business customers.

To further its bond with Charter sees an opportunity to enhance its business customers' wireless spending patterns through a new relationship it recently inked with T-Mobile.

"We're looking forward to getting to market and to small, medium and for us, large business space with the ability to enter into a market selling many more lines than we've been able to sell the ability to combine those mobile products with already our market and price leading wireline services that we have in small, medium and large businesses, I think, is attractive the same way it is for residential,” said Christopher Winfrey, president and CEO of Charter Communications.

A similar situation exists at Comcast.

Comcast, which has been bolstering its service set, continues to see growth with small businesses and enterprises, a trend that continued in the second quarter. The company reported that its business service segment revenues grew 6.3% during the quarter to $2.57 billion.

Last December, Comcast Business announced a deal to acquire network-as-a-service (NaaS) provider Nitel, deepening its cloud-based network capabilities.

Amidst increased competition from fixed wireless operators, Comcast Business is seeing greater SMB adoption of advanced services like cybersecurity and Comcast Business Mobile in the Enterprise solutions segment.

“This growing segment of our customer base has more complex needs, ranging from cybersecurity to multi-location connectivity, and they value integrated solutions and service reliability,” he said. “These are areas where we continue to invest and lead.”

Like Charter, Comcast sees potential in advancing its business mobile stance with its own agreement with T-Mobile.

Brian Roberts, CEO of Comcast, said that its relationship with T-Mobile will enable it to deepen its penetration with larger business customers.

“It was important for us to be able to use mobile in our relationships in the mid-market to win more share,” he said. “And the relationship with T-Mobile allows us to now do that in ways that we haven't been able to offer before.”

DIA dominance continues

As seen in earlier quarters, DIA (Dedicated Internet/Cloud Access) remained the fastest growing service in the U.S. on both ports and revenue.

DIA continues to resonate well with enterprise customers that desire a private, non-shared internet service for businesses that provides guaranteed, symmetric (equal) upload and download speeds with high reliability and uptime.

Another key trend is AI and GenAI. These services are driving requirements for highly secure Gigabit Ethernet connectivity.

However compelling DIA and GigE are, the research group noted that Ethernet will face “ongoing challenges for the Ethernet market include customer migration from switched Ethernet and MPLS services to carrier-managed SD-WAN and SASE.”

Service providers like AT&T, however, are responding to this trend.

AT&T recently joined forces with Cisco to launch the AT&T Secure Access Service Edge (SASE) with Cisco, a cloud-delivered networking and security solution, highlighting the growing adoption of cloud-based services.

For related articles, visit the Business Topic Center.

For more information on high-speed transmission systems and suppliers, visit the Lightwave Buyer’s Guide.

To stay abreast of fiber network deployments, subscribe to Lightwave’s Service Providers and Datacom/Data Center newsletters.

About the Author

Sean Buckley

Sean is responsible for establishing and executing the editorial strategy of Lightwave across its website, email newsletters, events, and other information products.

Voices of the Industry