NCTA: Cable’s broadband growth drive created a broad economic impact in 2024

Key Highlights

- In 2024, the cable industry delivered 59% of all fixed internet connections, serving 80 million broadband subscribers nationwide.

- The industry generated $568.7 billion in total economic output and supported 1.3 million jobs across the U.S., with broadband providers employing nearly 242,000 workers earning above the national average wage.

- Capital expenditures of $25.1 billion in 2024 fueled direct and indirect economic impacts, supporting thousands of jobs in construction, installation, and related sectors.

- State-level contributions vary, with California leading at $117.4 billion in total output and over 209,000 jobs supported, followed by New York, Texas, and Florida.

- Cable programming services significantly impact the economy, accounting for 44% of the indirect economic impact, with substantial benefits in consumer industries like retail and healthcare.

As the mix of Tier 1 and Tier 2 cable operators continues to expand their respective reach into more consumer and business locations. Cable’s role in the broadband arena is hard to overlook.

A new Chmura and S&P Global study commissioned for NCTA found that in 2024, the cable industry delivered 59% of all fixed internet connections, serving 80 million broadband subscribers nationwide.

The Investing in America 2024 – The Cable Industry’s Economic Impact on People, Infrastructure & Programming study examined the economic impact of the cable industry in 2024 across the U.S., all 50 states, and the District of Columbia, and all congressional districts.

Specifically, Chmura looked at the impact of two broad segments within the U.S. cable industry:

• Cable broadband connectivity providers: These service providers offer broadband internet, video, mobile and voice.

• Cable programmers: Services include cable TV networks and streaming services.

But the implications the study raises reflect the broader contribution that the cable industry has to the country’s economy.

In 2024 alone, the U.S. cable industry generated $568.7 billion in total economic output and supported 1.3 million jobs across the country.

Broadband economic impacts

Cable connectivity providers’ ongoing broadband build-out drive continues to have an impact on the broader economy through job creation.

In 2024, data collected from NCTA and its members showed that connectivity providers employed about 241,969 workers in the U.S., with an average annual wage of $103,496.

Chmura noted that “compared with a national average wage of $69,051 for all industries, an average broadband connectivity provider employee earns 50% more.”

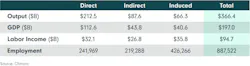

Further, the research firm estimated that the direct economic output (or revenue) of the connectivity segment was $212.5 billion in 2024, and the direct Gross Domestic Product (GDP) of the connectivity segment was $112.6 billion. Finally, the direct labor income (wages plus benefits) reached an estimated $32.1 billion in 2024.

While the initial figures related to GDP reflect the direct impact of the connectivity segment, the cable industry has what it calls an “indirect effect” on other industries. Chmura estimated the indirect impact was $87.6 billion in economic output and supported 219,288 jobs in the U.S.

Cable manufacturing, utility, transportation, and logistics services companies that serve the broadband industry are the indirect beneficiaries.

Chmura noted that cable programming service is “one particularly significant indirect impact for cable and broadband connectivity providers.” The research firm estimated that the purchase of cable programming services accounts for 44% of the total indirect impact.

Another factor is induced impact.

The induced GDP and labor income impacts were $40.6 billion and $35.8 billion, respectively. Chumra said the primary source of this induced impact is wages and salaries, resulting in the beneficiaries being concentrated in consumer service industries such as retail, food services, and healthcare services.

Capital spending effects

Capital spending was a key contributor to the economic impact.

In 2024, NTCA found that the U.S. cable industry invested a total of $25.1 billion in capital expenditures. This amount included $8.9 billion in line extension investments, $8 billion was on scalable infrastructure, $5.4 billion in customer premises equipment, and the remaining $2.9 billion was for support capital.

Chmura estimated that the industry capital expenditures generated $25.1 billion in direct economic output in the U.S., responsible for 67,978 jobs, mostly in construction and installation trades.

Further, Chmura estimated that the direct GDP was $15.5 billion and direct labor income was $7.9 billion in 2024.

Cable’s CapEx spending patterns also generated indirect and induced impacts in the U.S. The research firm estimated that the indirect impact was $7.8 billion in economic output that supported 18,336 jobs in the U.S., while the indirect GDP and labor income impacts were $4.0 billion and $2.0 billion, respectively. From an induced impact perspective, Chmura estimated that induced output was $11.4 billion, associated with 74,282 jobs in the U.S.

State-level impacts

From a state perspective, Chumra found that the cable industry’s economic contributions “varied widely across states, driven by population and industry presence within each state.”

California, New York, Texas, and Florida had the largest economic benefits. In 2024, California led all states with a total output (direct, indirect, and induced) of $117.4 billion and 209,086 jobs supported. New York followed with $91.8 billion in output and 165,530 jobs. Texas and Florida each exceeded $40 billion in total economic output, supporting over 100,000 jobs each.

Alabama also saw economic benefits. Chmura estimated that the operations and capital expenditures of the cable industry in the state generated $2.9 billion of total economic output, representing $1.6 billion in GDP and $0.8 billion in labor income. In addition, the operations and capital expenditures supported 8,917 jobs in the state.

“While cable broadband connectivity operations are distributed across the country, operations of cable programmers are primarily located in New York, California, and Georgia, thus contributing significantly to those states’ economies,” Chmura said in its study.

For related articles, visit the Business Topic Center.

For more information on high-speed transmission systems and suppliers, visit the Lightwave Buyer’s Guide.

To stay abreast of fiber network deployments, subscribe to Lightwave’s Service Providers and Datacom/Data Center newsletters.

About the Author

Sean Buckley

Sean is responsible for establishing and executing the editorial strategy of Lightwave across its website, email newsletters, events, and other information products.