Keeping up with production in the face of an 800G ZR/ZR+ pluggable surge

Key Highlights

- 800G ZR/ZR+ coherent pluggables are enabling a pay-as-you-grow, open, and disaggregated optical network model, significantly reducing costs and operational expenses.

- Demand driven by AI training, data center interconnects, and next-generation networks is fueling rapid adoption and forecasted multi-billion-dollar market growth.

- Technological innovations, including 3-nm CMOS DSPs and PIC integration, are enhancing capacity, power efficiency, and deployment flexibility of coherent pluggables.

- Supply chain challenges, such as laser shortages and long lead times for advanced DSPs, are creating bottlenecks that require strategic industry responses like vertical integration.

- Industry standards and multi-vendor interoperability are crucial for seamless deployment, increased choice, and accelerated network disaggregation across diverse optical infrastructure.

Coherent pluggables are shifting the optical industry to an open, disaggregated, "pay-as-you-grow" model while dramatically reducing capital and operating expenditures.

As the AI era drives the optical networking industry into a dynamic period of innovation, 800G ZR/ZR+ coherent pluggable optics stand out as one of the inflection points and the fastest-growing segments in optical infrastructure among emerging technologies. Coherent pluggables, such as 800G ZR/ZR+, are fundamentally redefining the economics of optical networking by shifting the industry to an open, disaggregated, "pay-as-you-grow" model while dramatically reducing capital and operating expenditures.

Market research firms and industry analysts alike highlight a surge in demand for coherent pluggables fueled by enterprise bandwidth requirements, 5G backhaul and next-generation IP and optical transport networks and driven by AI and cloud providers.

While figures differ by report, forecasts consistently predict that a multi-billion-dollar market will materialize over the next several years, with 800G coherent optics accounting for a significant portion of that growth.

Digging deeper into demand growth

Let’s look more closely at the main drivers:

- AI Training and Inference: The massive scale of AI model training, inference, and data movement between geographically-dispersed compute clusters is significantly increasing east-west and data center interconnect (DCI) traffic, driving demand for higher speed connectivity solutions. As a result, AI and cloud providers are accelerating deployments of 800G ZR/ZR+, which offer twice the capacity of the previous generation while reducing cost per bit and improving power efficiency.

- Improved network economics, enabled by technology innovation: Cutting-edge 3-nm-based Complementary Metal-Oxide-Semiconductor (CMOS) technology used by digital signal processors (DSPs) is a crucial enabler for the latest generation of 800G ZR/ZR+ coherent pluggables. Gate density surpassing 400 million gates and notable performance improvements over the previous generation of 400G ZR/ZR+ pluggables have resulted in lower power consumption and enhanced capacity-reach ratio. DSPs have also provided the processing power necessary to support advanced features such as probabilistic constellation shaping (PCS), a wide range of modulation formats, and high chromatic dispersion compensation, all in compact pluggable form factors, including QSFP-DD800 and OSFP. As a result, network operators can achieve better network economics, including lower capital and operating expenses, by leveraging pluggable modules that seamlessly integrate with existing routers, switches, or optical transport platforms.

- Broadened applications scope: The capability of coherent pluggables underwent a significant leap with the introduction of 800G ZR/ZR+. The application scope has expanded well beyond metro DCI due to higher bitrate and optical performance, simple, standardized Common Management Interface Specification (CMIS)-based management, open probabilistic constellation shaping, and multi-vendor interoperability. This unlocks applications once dominated by embedded coherent technology, including metro aggregation networks, backbone connectivity, AI clusters, any-haul DCI, and subsea applications.

- Enhanced deployability: While the IPoDWDM deployment model works for some operators and use cases, it isn’t suitable for all. Thin transponders simplify the operational model for deploying 800G ZR/ZR+ pluggables, enabling broader, more rapid adoption. Just like embedded transponders, thin transponders offer multiple client ports (100G, 200G, 400G, or 800G) to connect grey optics to routers and switches. They offer lower CAPEX, reduced power consumption and a smaller footprint compared to more traditional embedded optical engines, while mitigating IPoDWDM’s operational challenges of deploying coherent pluggables directly into routers. Thin transponders also deliver functional advantages of embedded transponders, including multiple client-side aggregation, operational domain separation, and some optical capabilities of fully fledged embedded transponders.

- Multi-vendor Interoperability: Like their 400G predecessors, 800G ZR/ZR+ coherent pluggable optics benefit from strong industry support and ecosystem interoperability. Common standards, test specifications and implementation guidelines have been established by multiple interoperability forums and multi-source agreements (MSAs). These industry efforts enable 800G coherent pluggable optics to interoperate seamlessly across a wide range of optical infrastructure, thus reducing or eliminating dependence on a particular vendor.

Multi-rate interoperability is one of the most valuable features of industry-leading 800G ZR/ZR+ due to its impact on network planning and operations. It provides numerous benefits for telecommunication providers, including seamless deployment with third-party pluggables and host devices, accelerated network disaggregation, increased choice, quicker service turn-up, and streamlined operations.

The supply chain challenge

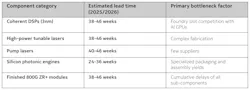

The increased functionality, coupled with the significant reduction in cost, space, and power per bit, is driving substantial demand for 800G ZR/ZR+ and pushing the global supply chain to its breaking point. Production of key components, such as the specialized 3nm DSPs and high-power tunable lasers, cannot keep pace with the sheer volume of orders from AI and cloud providers. Consequently, lead times have worsened as manufacturers grapple with the physical complexities of high baud rate optics and the thermal management requirements of dense form factors. The following factors can explain this persistent gap between capacity and consumption:

· The laser crunch: The most significant supply chain hurdle is a predicted shortage of the specialized high-power lasers used inside nano-integrable tunable laser assemblies required for high-speed optical transceivers. While less of a problem for indium-phosphide-based solutions, the optical transceivers based on silicon photonics technologies also require a laser pump, which is currently supply-constrained due to limited manufacturing capacity.

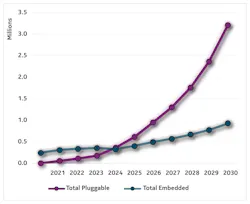

· Growing demand for capacity: According to Dell’Oro Group, over one-third of IPoDWDM revenue may be attributed to 800ZR/ZR+. Cignal AI further predicts 800G ZR/ZR+ will be the fastest-growing coherent pluggable shipments, with a 145 percent compound annual growth rate between 2025 and 2029.

· Advanced DSP and semiconductor lead times: 800G ZR/ZR+ pluggables rely on cutting-edge 3-nm CMOS technology for DSPs, where lead times could be more than nine months. This is because foundries often prioritize high-margin AI graphics processing units (GPUs) over optical components, creating a secondary bottleneck for transceiver manufacturers. As a result, lead times for 800G ZR/ZR+ components are one of the most significant friction points in the optical networking industry. While delivery times for standard networking hardware have returned to normal, the bleeding-edge nature of 800G coherent optics keeps lead times stubbornly high.

Manufacturing and yield challenges

Transitioning from 400G to 800G is not a simple linear upgrade. It introduces a new set of physical and testing hurdles, such as:

o Thermal management: 800G modules operate at the edge of thermal limits. Traditional aluminum or zinc alloys are often inadequate, requiring advanced alloys and thermal interface materials to prevent signal degradation.

o Testing bottlenecks: Validating 800G performance requires high-bandwidth oscilloscopes, test sets and signal generators. Low manufacturing yields on early optics under 100 Gbaud can significantly inflate costs and restrict supply.

Geopolitical and material risks

Besides technology, the optical industry faces a number of geopolitical and material risks.

Recent export controls on critical chipmaking minerals have put the supply-and-demand balance on a knife's edge.

While some government initiatives aim to diversify manufacturing, the concentration of advanced node production remains a high-risk factor for sudden disruptions.

PICs point the way forward

The rise of 800G ZR/ZR+ coherent pluggable optics is a pivotal shift in optical networking. Rapidly growing demand is straining supply chain infrastructure, creating bottlenecks. Vertical integration and additional investment in packaging and manufacturing capabilities will be critical to overcoming these supply chain limitations. Additionally, integrating DSPs with front-end optics, specifically photonic integrated circuits (PICs), will be a crucial tool for addressing supply chain bottlenecks by streamlining the manufacturing of 800G ZR/ZR+ modules.

Traditionally, these high-speed coherent pluggables have relied on fragmented ecosystems of discrete components (lasers, modulators, and receivers) sourced from multiple vendors, each with its own lead times and yield risks. By consolidating these functions into a single semiconductor chip or a unified package, manufacturers can reduce the number of components required and better meet the growing demand for next-generation pluggable optics.

About the Author

Rob Shore

Rob Shore is the head of optical networks solution marketing at Nokia. Shore has more than 30 years of telecommunications experience leading marketing efforts, providing networking consulting, promoting networking solutions and optical innovations, and directly supporting network operators in more than 65 countries worldwide. Rob has held roles in engineering, system testing, technical support, market management, account management, technical sales, and marketing. Rob graduated from the University of Illinois with a bachelor’s degree in computer engineering.