AT&T’s CFO sees business revenue potential in fiber and broadband wireless

Key Highlights

- AT&T's fiber and advanced connectivity revenues grew 6% year over year, driven by investments in fiber and broadband wireless services.

- Legacy wireline revenues declined 7.8%, but cost efficiencies helped reduce operating expenses, supporting overall business transformation.

- The company maintains the largest on-net fiber footprint in the U.S., bolstered by its acquisition of Lumen’s fiber assets, enhancing its market position.

- AT&T faces increased competition in SD-WAN from cable operators like Comcast, which has overtaken first place from the telco in the U.S. SD-WAN market.

- Strategic focus on value-added services, cloud security, and SD-WAN positions AT&T for continued growth despite legacy service pressures.

AT&T’s business services unit remains at a crossroads.

Being an incumbent telco, the service provider continues to battle legacy losses with its emerging next-gen fiber and wireless services offerings, like its fixed wireless Internet Air service, that reflect its business customers’ ongoing transition to cloud and virtual services.

As has been the trend seen in earlier quarters, AT&T’s Fiber and advanced connectivity service revenues for businesses grew 6% year over year, up from 3.5% growth in the second quarter due to its fiber and broadband wireless investments.

Speaking to investors during its third-quarter earnings call, Pascal Desroches, CFO of AT&T, said he expects these services to find further growth reflected in its fourth-quarter results.

“As we shared last quarter, we've been reinvesting some of our cost savings into driving improved growth in Fiber and fixed wireless, and our third quarter results reflect early traction with these efforts,” he said.

Legacy drags continue

Amidst its efforts to enhance its next-gen business services revenues, AT&T’s legacy drag continued into the third quarter, driven by continued secular pressures on legacy and other transitional services.

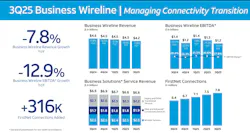

The service provider reported that its third-quarter Business Wireline revenues declined 7.8% year over year to $4.25 billion due to continued declines in legacy and other transitional services of 17.3%.

However, the losses were offset by 6% growth in fiber and advanced connectivity services. Within the business solutions services segment, Fiber and Advanced Connectivity Services and Wireless Services saw progress with $1.9 billion and $2.5 billion in revenues. Legacy and transitional services made up $2.2 million of revenues.

Due to lower personnel and customer support costs associated with ongoing transformation initiatives, operating expenses were down 1% year over year.

“While Business Wireline continues to manage through structural declines in legacy services, the team is doing a great job positioning the business to drive sustained growth in advanced connectivity services while operating more efficiently,” Desroches said. “Based on this solid execution, we continue to expect Business Wireline EBITDA pressures to moderate versus last year, with a full-year decline in the low-double-digit range.”

Fiber, wireless growth opportunities

Despite the near-term losses, AT&T has positioned itself to drive growth with its next-gen service set.

For one, AT&T has the largest on-net fiber business footprints in the U.S., one that will be bolstered when it completes its acquisition of Lumen’s fiber assets.

AT&T once again secured the top ranking on Vertical Systems Group’s 2024 U.S. Fiber Lit Buildings LEADERBOARD based on a substantial gain in new fiber installations. AT&T leverages that on-net fiber footprint to maintain a strong foothold in the U.S. Carrier Ethernet and optical wavelength markets.

Complementing its fiber network services, AT&T is a dominant player in the growing Software as a Service Edge (SASE) market, offering network security and SD-WAN services.

AT&T, through a partnership with Cisco Meraki, offers its Secure Access Service Edge (SASE), a cloud-delivered networking and security solution, a service that highlights the growing adoption of cloud-based services. The SASE service is designed to support a diverse set of business types—including mid-sized businesses with multiple branches and commercial enterprises modernizing legacy platforms to highly distributed global enterprises.

It is also a key player in the carrier SD-WAN market. However, AT&T's dominance in Carrier SD-WAN was challenged this year when it fell to second place behind Comcast on VSG’s 2024 U.S. SD-WAN LEADERBOARD after six years as the top carrier on the research group’s quarterly report.

Comcast, which has steadily risen in the SD-WAN market segment from its eighth position in 2018, illustrates the fact that cable operators are becoming viable competitors to large incumbents such as AT&T.

Nevertheless, AT&T can take its growing fiber assets, its experience in serving multinational companies, and its wireless capabilities to attract and retain business customers that have complex needs.

“Value-added services, which contribute about one-third of these revenues, can be variable from quarter to quarter, but we expect continued acceleration in our Fiber and fixed wireless connectivity revenues in the fourth quarter,” Desroches said.

For related articles, visit the Business Topic Center.

For more information on high-speed transmission systems and suppliers, visit the Lightwave Buyer’s Guide.

To stay abreast of fiber network deployments, subscribe to Lightwave’s Service Providers and Datacom/Data Center newsletters.

About the Author

Sean Buckley

Sean is responsible for establishing and executing the editorial strategy of Lightwave across its website, email newsletters, events, and other information products.

Voices of the Industry