AI scale-up raises the stakes for transceivers and CPO adoption

Key Highlights

- Sales of Ethernet optical transceivers and co-packaged optics are expected to reach $26 billion in 2026, reflecting a 60% growth rate.

- Major cloud providers plan to significantly increase their capex, with Meta and Oracle doubling their investments by 2026, impacting optical component demand.

- Supply chain shortages of VCSELs and InP lasers constrained shipments between 2023 and 2025, but improvements are anticipated by mid-2026, easing supply issues.

- Adoption of co-packaged optics for scale-up connectivity may surpass forecasts, potentially accelerating market growth in 2028-2031.

- Market growth is expected to moderate post-2026 due to capex normalization and supply chain stabilization, with a cautious outlook for the AI optics sector.

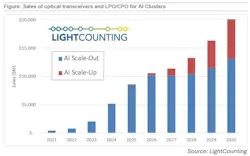

As cloud operators’ bandwidth needs for AI clusters continue to rise, so do sales of optical transceivers, linear pluggable optics (LPO), and co-packaged optics (CPO) for scale-out and scale-up networks.

LightCounting, in its recent “Optics for AI Clusters” report, estimates that sales of Ethernet optical transceivers (beginning with 100G) and CPO for scale-out and scale-up networks used in AI clusters reached $16.5 billion in 2025, and it will reach $26 billion in 2026.

The research firm said its forecast “corresponds to a 60% growth rate for both 2025 and 2026.”

The data center interconnection (DCI) technology market weighs technology options

While DCI continues to gain momentum, there appears to be no clear winner in the optical technology race yet. A recent Lightwave survey revealed that the market is awaiting a dominant technology. The research found that nearly half of respondents (48%) say no clear technology leader has emerged, illustrating that the DCI industry continues to weigh performance, cost, and interoperability issues. While co-packaged optics (17%) and next-generation pluggable optics beyond ZR/ZR+ (14%) are drawing interest, adoption appears cautious. Even established options like 400ZR and 800ZR/800ZR+ each capture just 10%, signaling that organizations are weighing multiple paths forward rather than committing to a single optical strategy.

CPO to capex correlation

Despite the momentum around CPO and optical transceivers, LightCounting took a sanity check on its forecast to account for capex spending.

While Meta and Oracle plan to double their capex in 2026, other companies have not updated their spending plans.

As a result, LightCounting said its “current assumptions may be conservative” and that it is “very likely that growth in spending will moderate in 2027-2031.”

The research firm noted that optics sales to the top five cloud providers will account for 3.1% of their capex in 2026 (up from 2.7% in 2025) and increase to 4.1% by 2031.

Cloud provider’s spending will focus on scaling up networking and on rapid growth in GPU bandwidth for both scale-out and scale-up connectivity.

“Adoption of CPO for scale-up connectivity can exceed our forecast and lead to a stronger growth for the market in 2028-2031,” LightCounting said.

Supply chain sanity

While Meta and Microsoft also reported their latest quarterly results and increased their 2026 capex projections, supply chain issues could be a factor.

Meta set its 2026 capex guidance at $115–$135 billion, a large increase from the $72.2 billion spent in 2025.

Likewise, Microsoft saw significant increases in capex. Driven by AI infrastructure demand, Microsoft reported an 89% year-over-year increase in capex to $29.88 billion for Q2 FY2026.

“The sky seems to be the limit for their spending, but supply chain shortages restore some sanity,” LightCounting said.

Overall sales of AI infrastructure products were constrained by supply chain shortages between 2023 and 2025.

Shortages of VCSELs and InP lasers limited shipments of optical transceivers. However, the VCSEL segment bounced back in mid-2024 as Nvidia moved away from SR8 and adopted DR8 800G transceivers. Meanwhile, InP laser chip suppliers increased capacity in 2025.

“We expect the shortages to ease by mid-2026, which is great news for customers, but it is a double-edged sword for suppliers,” LightCounting said. “They can ship more, but the demand tends to drop when shortages go away.”

Looking forward, LightCounting does not foresee a downturn, but the market might see a flat quarter or two late this year. As a result, the research firm has “forecast moderation in the market growth for 2027-2031, assuming an eventual return to sanity among the top cloud companies.”

For related articles, visit the Optical-Tech Topic Center.

For more information on high-speed transmission systems and suppliers, visit the Lightwave Buyer’s Guide.

To stay abreast of fiber network deployments, subscribe to Lightwave’s Service Providers and Datacom/Data Center newsletters.

CPO M&A accelerates

As momentum for CPO grew, vendors pursued key M&A deals to shore up their positions in the market segment over the past year. Marvell moved to acquire Celestial AI, a next-generation CPO vendor, for $3.25 billion, and later XConn to broaden its data center switching portfolio with PCIe and CXL products. However, Ciena shelled out only $270 million for Nubis Communications, another co-packaged optics start-up, in September 2025. Celestial AI’s technology is based on photonic interposers, which are similar to Lightmatter's approach. Both Celestial AI and Lightmatter raised several million dollars in funding in early 2025.

About the Author

Sean Buckley

Sean is responsible for establishing and executing the editorial strategy of Lightwave across its website, email newsletters, events, and other information products.

Voices of the Industry